Overview

New York State has enacted a new pied-à-terre tax (surcharge) on certain high-value New York City homes (“covered properties”) NOT used as a primary residence. “Covered properties” include Class 1 homes (one-, two-, and three-family homes) and Class 2 homes (residential condominiums and cooperatives (co-ops)). The surcharge takes effect on July 1, 2026. It will appear on the property’s New York City statement of account and is scheduled to expire on June 30, 2031.

Phase One

- Phase one applies from July 1, 2026, through June 30, 2028.

- The surcharge is imposed on Class 1 homes valued at $5 million or more based on comparable sales. There are three tax rates based on comparable sales value.

- 0.80% ($5 million to $15 million).

- 1.05% (over $15 million to $25 million).

- 1.30% (over $25 million).

- The surcharge is imposed on Class 2 homes valued at $1 million or more. During Phase One, the market value thresholds and rates for condominiums and co-ops are based on the New York City Department of Finance’s (the “Department’s”) current rental-income-based imputed market value methodology. For co-ops, during Phase One, the Department determines the total building imputed market value. The imputed apartment value is assigned to each apartment based on each tenant-stockholder’s shares in the co-op. Like the regular property tax assessment, the Department will bill the building for the surcharge on all non-exempt apartments. The co-op board will then assess the affected shareholders for their share of the surcharge. There are three surcharge rates.

- 4.00% ($1 million to $3 million).

- 5.25% (over $3 million to $5 million).

- 6.5% (over $5 million).

Phase Two

Phase Two begins on July 1, 2028. During Phase Two, the surcharge thresholds and rates are unified for non-exempt Class 1 and Class 2 homes. The Department is expected to apply a comparable-sales-based methodology to condominium and cooperative units so that the unified thresholds can be applied more consistently across property types.

- 0.80% ($5 million to $15 million).

- 1.05% (over $15 million to $25 million).

- 1.30% (over $25 million).

The Primary Residence Surcharge Exemption

The tax applies only if the property is not a primary residence. A property generally will be treated as a primary residence if it is occupied as the main home for more than half of the calendar year by the owner, certain immediate family members, or a tenant (“covered persons”) under a bona fide arm’s-length lease of at least one year. The tax also looks through certain ownership structures for purposes of applying the primary residence rule. For example, “covered persons” may include sole beneficial owners of trusts and majority partners, shareholders, and members of entities that own covered property.

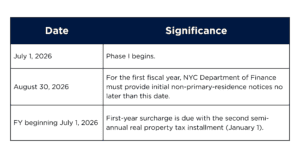

Beginning with the fiscal year starting July 1, 2026, the Department will annually determine by August 30 whether the primary residence exemption applies and will issue notices for properties it determines are not exempt. Covered owners may challenge the Department’s determination by providing proof that the covered property is their primary residence.

Proof of Primary Residence Status for the Surcharge Exemption

To document primary residence status, the law expressly authorizes the use of New York State resident tax returns showing a New York City permanent home address, the allowance of a prior fiscal year STAR exemption, and receipt of the homeowner tax rebate credit. Additional proof may include an arm’s-length lease of at least one year to a tenant for whom the home is a primary residence, use by an immediate family member (spouses, parents, children, siblings, grandparents, or grandchildren) as a primary residence, and evidence that a covered person occupied the covered property for a majority of the days in a calendar year.

Excluded Property

The surcharge does not apply to certain newly built properties that have not yet received the required certificate of occupancy, or to unsold condominium and cooperative units still held by the sponsor under an offering plan. The surcharge does not apply to commercial property.

Key Dates and Compliance Timeline

*New York City fiscal year 2027 commences on July 1, 2026, and ends on June 30, 2027.

What to Do Now

- Identify covered properties and covered persons.

- Identify legal or beneficial owners of covered homes held by trusts, corporations, limited liability companies, and partnerships.

- Determine whether the primary residence exemption applies.

- Gather documentation to support the primary residence exemption by August 30.

If you would like help evaluating whether a specific property may be subject to the surcharge, please contact your SAX Advisory Group state and local tax adviser.

This alert is for general informational purposes only and does not constitute tax or legal advice. State and local tax law changes frequently – verify current law with a New York tax professional before acting.